You’re making sales. You’re busy. But is your business actually making money?

As a small business owner, gut feeling is something you have to rely on often. But being busy doesn’t mean you’re profitable. High turnover doesn’t guarantee a healthy business. And following your intuition isn’t a substitute for knowing your numbers.

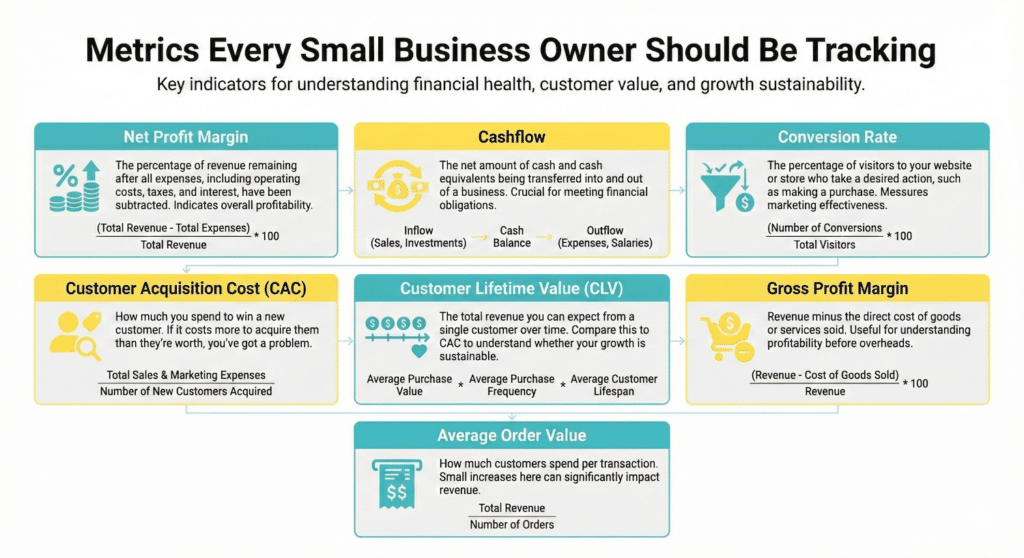

Number one: Net Profit Margin

You don’t need a finance degree to get clarity. You need to track three numbers consistently.

Your net profit margin is what’s left after all your expenses have been paid. Not your revenue. Not your gross profit. What’s actually in your pocket after everything is accounted for.

Calculate it by taking your net profit (total revenue minus all expenses) and dividing it by your total revenue. If you made R100,000 and your expenses totalled R85,000, your net profit margin is 15%.

This number matters because it’s a comprehensive indicator of your company’s financial health. A declining margin is a warning sign, your costs are creeping up, your pricing isn’t keeping pace, or you’re spending more to acquire each customer. The fix isn’t always to sell more, it can be to manage your expenses better.

Number two: Cashflow

You can be profitable on paper and still go out of business.

Profit is a calculation. Cashflow is reality. It’s the actual movement of money in and out of your business, and crucially, when that movement happens.

Imagine landing a R50,000 client who pays on 60-day terms. On paper, great month. But your rent, suppliers, and staff need paying now. That invoice doesn’t help if it’s sitting in someone else’s account while your obligations pile up.

Healthy cashflow means at the end of every month, you’ve got enough to cover expenses with something left over. You’re not chasing invoices or dipping into savings. Track it monthly and you’ll spot patterns, negotiate better terms, and prepare for lean periods instead of being blindsided by them.

Number three: Conversion Rate

How many of your leads are becoming paying customers?

If 100 people visit your website and 5 make a purchase, that’s a 5% conversion rate. The number varies by industry, but what matters is that you know yours and whether it’s improving.

A low conversion rate is a leak in your bucket. You can pour in as many leads as you want, but if they’re draining out the bottom, you’ll never fill it. Maybe your website isn’t clear. Maybe your follow-up is too slow. Maybe your pricing confuses people. You can’t fix what you’re not measuring.

Improving conversion is high-leverage work. It means predictable growth without constantly scrambling for new leads.

How Online Tracking Helps You Measure What Matters

You don’t need to track these metrics manually. The right tools, properly set up, can give you real-time insight into how your business is performing.

Google Analytics shows you exactly where your website visitors come from, how they behave on your site, and where they drop off. You can see which pages convert and which ones lose people. If your conversion rate is low, Analytics will help you pinpoint where the leak is happening.

Payment gateways and e-commerce platforms like Payfast, Shopify, or WooCommerce track every transaction automatically. You can pull reports on revenue, average order value, and sales trends over time—all of which feed into your profit margin calculations.

CRM systems track your leads from first contact to closed sale. You can see how many enquiries came in, how many converted, and how long the process took.

Accounting software like Xero, QuickBooks, or Sage connects to your bank accounts and categorises income and expenses automatically. You can generate profit and loss statements, track cashflow in real time, and spot trends before they become problems.

Email marketing platforms show you open rates, click-through rates, and which campaigns actually drive sales. When you connect these to your website tracking, you can trace a customer’s journey from the first email they opened to the purchase they made.

The power is in connecting these tools. When your website, payment system, and accounting software talk to each other, you stop guessing and start seeing the full picture. You know exactly what’s working, what’s leaking, and where to focus your energy.

Other Metrics Worth Tracking

Once you’ve got the fundamentals covered, these additional metrics can give you deeper insight:

- Customer acquisition cost (CAC): How much you spend to win a new customer. If it costs more to acquire them than they’re worth, you’ve got a problem.

- Customer lifetime value (CLV): The total revenue you can expect from a single customer over time. Compare this to CAC to understand whether your growth is sustainable.

- Gross profit margin: Revenue minus the direct cost of goods or services sold. Useful for understanding profitability before overheads.

- Average order value: How much customers spend per transaction. Small increases here can significantly impact revenue.

- Churn rate: The percentage of customers who stop buying from you over a given period. High churn means you’re constantly replacing lost business.

- Accounts receivable ageing: How long invoices sit unpaid. The longer they age, the less likely you are to collect.

Stop guessing. Start measuring. These numbers won’t just tell you how your business is doing today, they’ll tell you whether it’ll still be here in five years.